Reaching for the T.O.P: The DAO Equivalent of an Employee Stock Option Plan

DAO contributors do not have visibility of a pot of gold beyond the rainbow that matches stock options in a traditional startup. We propose a solution.

A. Governance mining

“Governance mining” has recently received more attention from a number of decentralized projects such as Balancer, MakerDAO, PieDAO and Curve Finance, amongst others.

The idea of governance mining is that a set proportion of newly minted tokens is earmarked for distribution to those who contribute to a project’s governance.

For instance, A Balancer community proposal of November 2020 suggested earmarking a ”small proportion” (~3k BAL of the 145k BAL then distributed weekly, or just over 2%) for a Governance Mining program.

The way extra tokens could be earned was majorly by showing recidivist voting behavior (called “GovFactor”) and from contributing to Balancer’s Discord.

The latter borrowed from MakerDAO’s SourceCred experiment which aimed to distribute extra MKR to those who make quality contributions to its community forums.

Other projects too, typically in the decentralized exchange space, such as PieDAO and Curve Finance have posted proposals that would seek to reward contributors by way of a token “multiplier”.

From studying these early governance mining proposals, we see three fundamental shortcomings:

Too narrow: Typically, only liquidity providers qualify for token multipliers, leaving contributors who do not provide liquidity to the protocol but help in other ways without an incentive mechanism.

Human factor: All proposals struggle with how contributions beyond loyal voting could be quantified. Should somebody who actively posts on your Discord be awarded more tokens than s/he who posts sparingly but contributes higher quality?

Creeping centralization: Who judges about the quality of contributions anyhow? All governance mining proposals we’ve seen default back to some “Governance Committee” with powers to allocate the newly minted tokens. Quickly, such mechanism gets stuck into issues around who sits on such Committee, wether they should be elected, and how they can be voted out. Generally, there is an unease about the potential centralization from the delegation of award decisions to a Committee.

In what follows, we examine each of the above with the aim to come up with a workable design.

1. Too narrow

Balancer’s “GovFactor" idea is attractive in that it simply looks at liquidity providers’ addresses who have voted on the most recent proposal on Snapshot and then adds a multiplier to their weekly liquidity mining allocation. Other projects have proposed a broadly similar approach.

However, as Jacob Phillips points out, currently, liquidity mining schemes that were supposed to be allocating tokens to “users” of a protocol are really just being arbitraged by funds and prop shops who farm and dump tokens for profit.

In other words, liquidity is bootstrapped, but the community is not. Rather than just mining liquidity, DAOs should be mining contributors, human capital, and governance activity

If DAOs are going to operate at the level demanded by unicorns in the traditional startup space, they can’t be relying on part-time contributors with alternative priorities. They will need full-time developers, product experts, strategy/biz dev specialists, security/QA engineers, customer support personnel, etc.

2. The human factor

A second weakness of governance mining is that currently - and perhaps generally - there is no good heuristic to judge the quality of community members’ contributions.

Programmatic awards only go that far in recognizing different types of contributions to the network. Most token awards will inevitably involve a degree of human judgement.

MakerDAO made a brave attempt to quantify “SourceCred” for its community forums however the initiative seems to have stalled late last year.

As seen above, Balancer too initially had grand ambitions for its governance mining programs but seems to have stuck to a narrow “GovFactor” scheme that earmarks a small % of newly issued BAL to liquidity providers (and only liquidity providers) who show loyal voting behavior.

3. Creeping centralization

In an attempt to keep tokens awards fair, governance mining proposals quickly default to some form of “Governance Committee” of “experts” or “curators” who pass judgement on who deserves extra tokens.

However here too, suspicion seeps in as to how such Committee is composed, whether it should be elected and how, and how to remove members.

For instance in the case of Balancer, the BAL token budget earmarked for the governance scheme was to be sent directly to a Governance Committee who would decide on allocations and distribution schedules.

This Committee was to be made up of a fixed number of participants, consisting of an equal split between team, investors, partners and community members.

This quickly lead to concerns from the Balancer community about how Committee members would be elected and removed. Additional questions were raised e.g. about if and how Members of the Committee should be compensated.

The general perception is that delegation quickly descends into centralization, and that too much power in the hands of a Governance Committee is irreconcilable with the goal of radically decentralized governance.

B. Our proposed solution: An onchain Token Option Plan (“TOP”)

In summary, governance mining in its current design does not put a predictable, fair and quantifiable token reward scheme in place for the benefit of all those who build and commit to a decentralized project in a sustained way.

The initial Lead team often enjoys an early payday from the project’s pre-mine but does not have incentives to stick around. Contributors generally do not have visibility of a pot of gold beyond the rainbow.

As a result, there is a real risk that most DAO’s lives will be short and brutish: constantly under threat from being rug-pulled and with no dedicated team to fall back on, most DAOs risk dying an early death.

How can we get a subset of the community to commit to a specific project for the longer term? In other words: how do we build a team?

The answer is probably: The same way traditional startups secure talent.

As is widely known from popularizations of the startup world (watch e.g. Silicon Valley), startups give options to their employees, under an Employee Stock Option Plan (“ESOP”), with early joiners receiving higher awards than later employees.

Our proposed solution is to take the best of such battle-tested ESOPs, take out the element of central decision making in how token options are awarded, and commit the option vesting and exercise mechanism to a self-enforcing smart contract that replaces the analog award agreement.

By way of reference, we have used a template we commissioned from Cooley, OtoCo’s U.S. counsel, of a typical ESOP (or Equity Incentive Plan) for a U.S. C-Corp, the most widely used company structure for a technology startup.

As can be seen, such agreement has many subtleties but as a repository of best practices developed over decades of venture building, we believe it provides a good starting point from where to innovate.

The below is also the way we plan to implement our Token Option Plan for the OtoCo community:

1. The pool and the TOP’s lifecycle

First, a pool of tokens will be earmarked over which options can be written.

It is very important that, as with a traditional ESOP, there is visibility as to how many tokens are pledged to the TOP.

This will give option holders a sense of their ownership as a percentage of all issued tokens, in the same way that employees of a startup measure their total compensation as salary + options over the the total of the company’s issued stock (a.k.a. "fully diluted” options rewards).

Such calculation is easy in projects that have a fixed number of tokens under a capped token inflation model.

However, it is a bit more difficult to calculate for projects that continuously mint tokens (such as OtoCo itself), as there is no fixed amount of tokens over which I can compute how many tokens I will eventually hold as a % of the total.

In such scenario, if I am issued a fixed number of options, I will be continuously diluted, which may be demotivating.

Therefore, it is better to dynamically express the tokens pledged to the TOP as a % of all tokens as they are being mined.

In such scenario, a portion of all newly minted tokens automatically goes into the TOP to continuously replenish the option pool. In turn, this will protect me as an individual option holder issued with a % claim on the size of the overall pool.

Here again the logic is not very different from a traditional ESOP which typically gets replenished with every funding round, which in a company is done by issuing new stock to investors. As part of such round, a set % of new stock is typically earmarked for a new ESOP to reward existing and new employees.

In our envisaged smart contract design for the TOP, there are two main roles:

DAOwhich represents the DAO’s onchain governance protocol. Transactions signed by this role are deemed to be executed by the OtoCo Foundation in case of OtoCo’s TOP deployment.Contributorwhich corresponds to the community member receiving and exercising options.

Contributor’s life within the TOP starts when the DAO offers him/her options. Signing the offer onchain using the new signing feature in OtoCo starts his/her contribution period (the so called issue date).

If Contributor ceases making contributions, s/he goes into a terminated state which also stops the vesting of his/her token options.

Contributor may be also terminated by the DAO in which case s/he is removed from the contract.

Finally when conversion happens (e.g. the Contributor decides to exercise his/her vested tokens), Contributor enters the converted state.

The envisaged states in the contract are:

WaitingForSignature: The Contributor needs to sign the TOP agreement.Contributing: Contributor has signed the agreement and activated the TOP smart contract. This is the main state for the duration of the Contribution.Terminated: The Contributor leaves the project or his/her services are terminated. Similar to a traditional ESOP, the contract would distinguish between two types of terminating events:GoodLeaver: The Contributor leaves, but keeps options subject to fade-out of their vesting (i.e. no new options are awarded but existing options remain intact).BadLeaver: The Contributor leaves and forfeits further vesting. All unvested options fall back into the pool. Optionally, tokens from option exercise can be repurchased at a pre-set valuation.

OptionsExercised: When the Contributor or the DAO decides, options can be converted into tokens at the exercise price. Once done, the Contributor goes into theconvertedstate.

The TOP itself would have a simple lifecycle:

When deployed, it is in

newstate.It changes to

openby providing configuration parameters byDAOrole. At that point, terms for all Contributors can be parametered.When there is a conversion event,

DAOwill switch the TOP into theconversionstate during which options are exercisable. Each award will be separately configured per Contributor.

2. Assigning new options

Options would be assigned to Contributors in two ways:

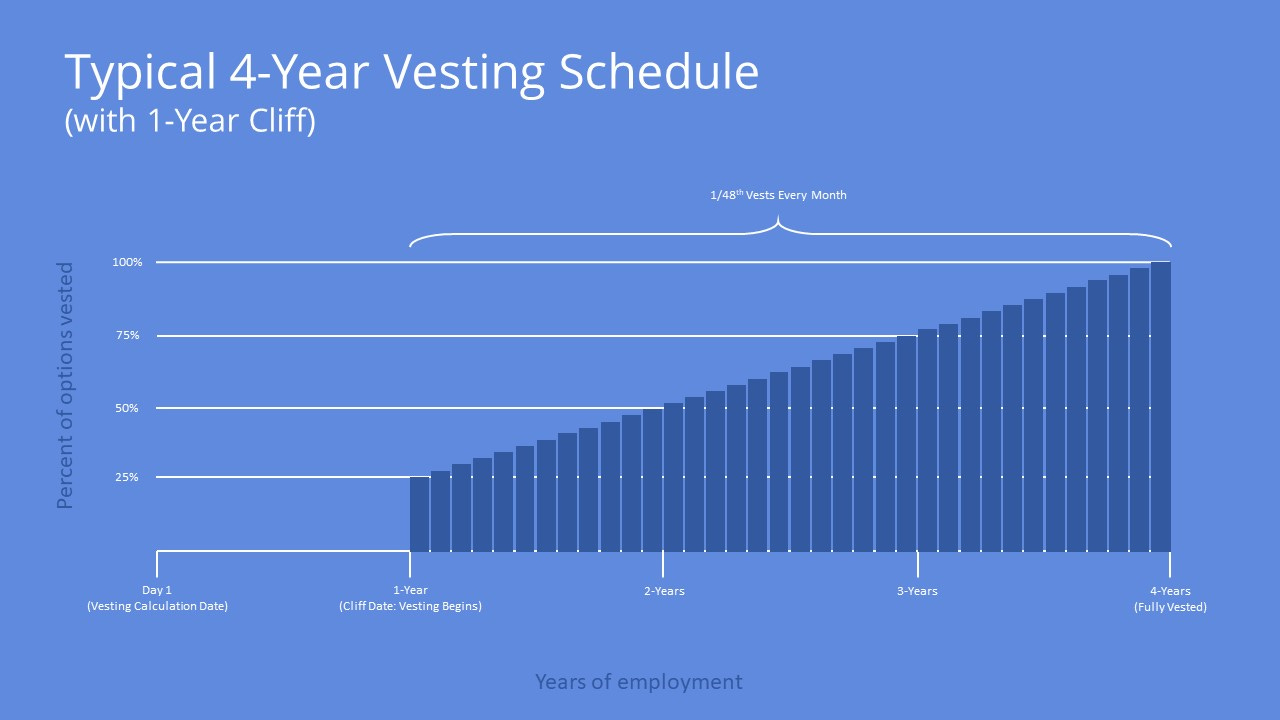

pool options: these would be the equivalent of non-discretionary options in a traditional ESOP and vest according to Valley terms (monthly vesting over 4 years with a 1 year cliff). This means that as long as the Contributor remains involved with the project, his/her options will be programmatically vesting.extra options: These represent a pool of options that can be issued at the discretion of the DAO.

Pool options and extra options can be combined for the same Contributor. In addition, more options will be issued to earlier Contributors as a % of the total available tokens in the pool, as as recognition of the opportunity cost for committing to an early project.

3. Contributor’s vesting

Vesting will be programmed at the individual option award level. For non-discretionary options, vesting will be algorithmically. For extra (discretionary) options, it will be subject to an action by the DAO.

During the cliff period (typically 1 year), Contributor’s options do not vest. However this too is is configurable and can be set to zero.

When vesting period starts, Contributor receives all “rolled-up” options that vested over the first year and monthly vesting commences up to the total of options awarded.

Finally, there will also be an accelerated vesting function.

4. Why options over tokens rather than direct token awards?

There are a number of reasons why we favor writing options (in tokenized format) over the OTOCO token as a reward to contributors rather than awarding contributors tokens directly:

The OTOCO token’s price is expected to lead a life of its own. This means a straight token award will always be referenced to the price of the token at the moment of the grant. By contrast, a TOP has an exercise price which can be set at any level, and it is up to the token reward holder to judge when is a good time to exercise once vested.

A TOP does such vesting more elegantly compared to a straight token award: our TOP smart contract simply “drip-feeds” tokens into contributors’ wallets if and when their token award vests, and does so for each option award holder individually, instead of having to create different time locks at the native token level for each contributor.

There is a token option exercise price which, as with an ESOP, will require option holders to pay for the exercise of their options. This should help reduce the moral hazard from free token awards. No pain no gain!

The options could conceivably be traded separately from the OTOCO token itself, the same way options over legacy assets discover their own price, thereby creating extra liquidity.

ESOPs have been battle-hardened and best practices have emerged that are generally perceived as balanced and fair, allowing a smart contract TOP to be backed-up by legal precedent. By contrast, a fair number of initiatives in the governance mining space have been busy reinventing the wheel and quickly discovered that whilst governance mining may be conceptually easy, it easily cascades into subsets of issues that need to be clearly articulated. Most of these issues relate to how to take the subjectivity out of the whole process.

The role and powers of the traditional Board in an ESOP (see section 2 of the ESOP template) will be replaced by an onchain vote by all OTOCO token holders. These powers include the appointment and removal of Members of a Remuneration Committee, to which the Board of a traditional startup typically delegates the granting of options and the administration of the ESOP. Such setup maintains full decentralization in how the TOP is designed and introduces a high degree of accountability for a sub-set of token holders on the Committee.

Conclusion

The risk with innovation for innovation’s sake is that it may throw the baby out with the bath water.

Best practices around Employee Stock Option Schemes have emerged and have been honed over decades of venture building in Silicon Valley and beyond.

Our proposal is to take the best of such battle-tested ESOPs, take out the element of central decision making in how token options are awarded, and commit the option vesting and exercise mechanism to a self-enforcing smart contract that replaces the analog award agreement.

We welcome any input from the community and invite anybody who wants to receive the first OTOCO token option award by helping our coding effort to email us at community@otoco.io.

Join our OtoCo official Telegram channel today to for all updates.